Equities Are A Forgiving Asset Class

Are they?

Let us start with a story. In the 1970’s, the United States had an informal group of 50 large cap stocks that were termed as the Nifty 50 and were all the rage back then. The index comprised of many popular names like American Express, Coca-Cola, IBM, General Electrics, Walmart, etc. The pendulum swung to the extremes leading to price earnings of the index trading at more than 50 times and a lot of stocks were trading as high as 100 times earnings.

The high valuations eventually led to losses for many as the bear market started in 1973-74. Many stocks lost more than 50% in valuations.

Now imagine you were one such investor who bought all the 50 stocks equally. We will also assume that 49 out of 50 stocks went kaput and only one survived and you held on to the stock till today. Walmart. You would have beaten the S&P 500. From 1 January 1973 till Jan 2025, the stock has returned 18% in annualised returns. The stock corrected by 61% in 1973 and then by another 29% in 1974. Most of us would have sold and exited everything.

Even with an error rate of 98%, you can win with equities provided you reduce activity and increase time horizon. Equities are a forgiving asset class.

(You might be thinking that this strategy has not worked in Japan, China, etc., please do read till the end)

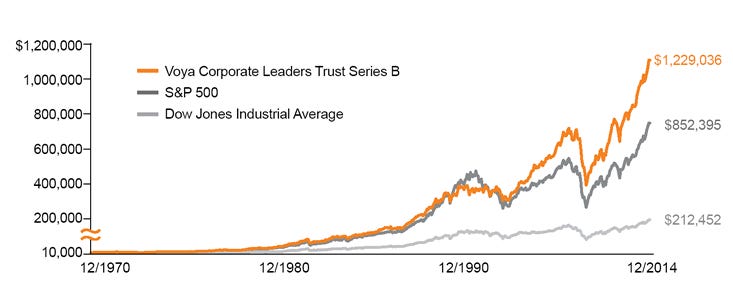

Another interesting story comes from the Voya Corporate Leaders fund that was established in 1935 with a 30 stock portfolio. No changes have been made in the fund thereafter. The fund continues to survive till today holding around 22 stocks and has generated inflation beating returns. The fund has beaten S&P 500 from 1970 to 2014 and has continued to match its returns till 2023.

Coming to Indian markets, the buy and hold strategy has worked reasonably well here as well. You may be the unluckiest investor who only buys once and never buys again. Look at the data published by mint below, you made positive returns irrespective of buying just before the Harshad Mehta market crash, dot com crash, or the 2007 crash.

Buying once and holding strategies have worked well in the American and Indian markets. However, you may say that Japan has not given positive returns in 30 years. This is not true. 30 years real returns from the Japanese markets have been positive.

Let’s be practical. No one in the real world just invests once and forgets. We all earn monthly income and have a surplus to allocate every month. When we see the SIP data of most markets, barring China and Hong Kong, almost all major markets have generated positive real returns. In fact, Japan SIP returns were as much as the US.

With everything mentioned above, I would like to highlight certain things.

Earnings growth matters - More than economic growth, the underlying earnings growth of the companies matters. One key reason for lower returns from China has been poor earnings growth. Refer the below data, the EPS growth is just 10% in the Chinese markets vs the Indian markets. Even Japanese companies have growth their EPS at a healthy rate. In fact, Japanese markets hit all time highs recently on the back of such earnings growth.

SIP over One time investing - Nobody just invests once. If you are a retail investor like me who invested monthly, you would have made money even from the Japanese markets in the last 30 years. Refer the data below where an investor made a monthly investment of $833.33 in Japan vs doing a one time investment of $300,000 in 1989.

Valuations matter - We must also consider market valuations and sometimes, act. If we stayed invested in the Japanese markets in 1989 when they were trading at exorbitant valuations, the problem is with us. Same goes for the past bubbles seen in the Indian and US markets. We need to use asset allocation strategies as well to generate better returns. An investor who only invests in equities, must time exits and some times take money off the table.

Active strategies over index investing - Another important but hard to understand factor is index divisors. I will excuse myself and let Harish Krishnan do the explanation. Read here. Major learning here is that an active strategy would work better than a passive index based strategy simply because the fund manager can control lots of variables. An index does not have that control and is prone to various forms of tinkering.

This brings us to the ultimate question - are equities really forgiving or we are suffering from hindsight bias. I think so. The below list definitely matters -

Buy big when valuations are cheap.

Remain patient, start early, have extremely long time horizons.

SIPs work, continue them. You cannot stop SIPs as you please.

Markets do not guarantee any returns. Follow asset allocation.

Accept the fact that markets are volatile. Future returns are a confluence of many variables.

Investing is not just about knowing where to put your money — it is equally about knowing where not to put it.

Survival is the only road to riches.

Data sources -

Thanks for reading. Kindly excuse errors, if any. The data gathered is off the internet from various sources and could be prone to errors. Please do highlight better publicly sources.

📚 My favourite books and gadgets

𝕏 Twitter

▶️ Youtube

📝 Sign up for my paid newsletter focused on credit cards and rewards

📈 10% discount on portfolio tracker I use - MProfit

💍 10% discount on the Ultrahuman ring